Understanding Reverse Charge VAT Between Contractors and Subcontractors

In the UK construction industry, VAT treatment can be a tricky subject—especially when it comes to transactions between contractors and subcontractors. Since March 2021, the Domestic Reverse Charge VAT rules have significantly changed how VAT is handled for certain construction services. These rules primarily target fraud prevention and apply under the Construction Industry Scheme (CIS).

If you’re a contractor or a subcontractor, it’s crucial to understand when the reverse charge applies, and when it doesn’t. This blog breaks down the rules simply, explaining VAT treatment for labour, materials, or both.

What is Reverse Charge VAT?

Reverse charge VAT is a system where the customer (contractor), instead of the supplier (subcontractor), accounts for the VAT. Rather than the subcontractor charging VAT on the invoice and paying it to HMRC, the contractor calculates and pays VAT through their own VAT return.

This method does not affect the amount of VAT ultimately paid or reclaimed, but it changes who reports the VAT. It reduces the risk of VAT fraud in the supply chain.

When Does Reverse Charge Apply?

Reverse charge applies when:

-

The supply is for construction services under CIS.

-

Both contractor and subcontractor are VAT-registered.

-

The supply is standard or reduced-rated.

-

The customer is not an end user.

If these conditions are met, the subcontractor does not charge VAT on the invoice.

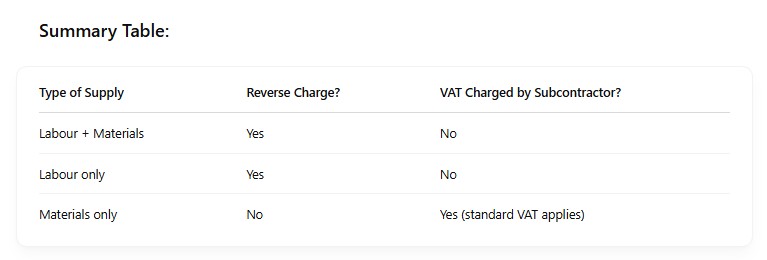

Labour and Materials Supplied Together

When a subcontractor provides both labour and materials as part of a construction service, the whole supply is treated as a construction service, and reverse charge applies.

The subcontractor must:

-

Invoice the full amount without VAT.

-

Include wording on the invoice such as:

“Reverse charge: customer to account for VAT to HMRC.”

Example:

A subcontractor supplies labour (£3,000) and materials (£2,000). The total invoice is £5,000, with no VAT added. The contractor accounts for the £1,000 VAT (20%) on their return and can reclaim it if eligible.

Labour Only

If the subcontractor only provides labour (e.g., bricklaying or plastering), the reverse charge still applies.

Labour-only services fall under construction services as defined in CIS.

Example:

Labour-only invoice of £4,000 should be issued without VAT. The contractor deals with VAT accounting.

Materials Only

This is where things change. If the subcontractor only supplies goods (such as selling materials without installation or fitting), the reverse charge does not apply.

This is a normal VAT transaction. The subcontractor must charge VAT at the applicable rate.

Example:

Materials-only invoice of £2,000

VAT @ 20% = £400

Total Invoice = £2,400

Contractor pays this in full and reclaims VAT on their return if eligible.

Important Considerations

-

If the contractor is classed as an end user (e.g., a property developer using the services themselves), reverse charge does not apply.

-

Zero-rated supplies (e.g., new residential builds) are outside the scope of reverse charge.

-

The subcontractor should always check the status of the customer and retain evidence.

-

The invoice must clearly state the reverse charge and not show VAT as payable.

1. Who is an “End User” in Reverse Charge VAT?

An end user is a VAT-registered business that:

-

Receives construction services,

-

Does not make onward supplies of those services,

-

Uses the services for its own use—not to sell them as part of construction services to someone else.

This typically includes:

-

Developers

-

Property owners

-

Large businesses building their own premises

-

Landlords who commission works for rental properties

So, if a developer hires a subcontractor to build homes for sale, the developer is using the services directly and is considered an end user.

2. How Does End User Status Affect Reverse Charge VAT?

If the contractor is an end user, then:

-

Reverse charge does NOT apply.

-

The subcontractor charges VAT as normal on their invoice.

-

The contractor (end user) reclaims the VAT through their own VAT return if eligible.

Important:

The end user must notify the subcontractor in writing (email or letter is fine) that they are acting as an end user. Without this, the subcontractor must assume that reverse charge applies.

3. What if the Supply is Zero-Rated (e.g., New Builds)?

Zero-rated supplies, such as qualifying new residential buildings, are outside the scope of reverse charge because:

-

The VAT rate is 0%, so no VAT is charged.

-

The subcontractor simply issues a zero-rated invoice.

In this case:

-

Reverse charge rules don’t apply, regardless of whether the contractor is an end user or not.

-

The subcontractor does not charge VAT, but the reason is because of the zero-rating, not reverse charge.

Conclusion

The introduction of reverse charge VAT has added complexity to VAT compliance in construction. However, understanding the core rules makes it manageable. If you’re supplying labour only or labour with materials, the reverse charge applies. If you’re supplying materials only, then it’s standard VAT.

Make sure your invoices are correctly formatted and that you check your client’s VAT and end user status. Following the right VAT treatment ensures compliance and avoids penalties.

Need help applying these rules to your situation? Get professional advice to stay on the right track.

https://etaxfiling.co.uk/vat-reverse-charge/

If you would like further assistance with this or anything else, please get in touch, contact us for expert assistance.