Listen to our podcast for a comprehensive discussion:

The Audio Summary of the Key Points of the Article:

The Audio Summary of the Key Points of the Article:

Listen to our podcast for a comprehensive discussion:

Understanding UK Resident and Non-UK Resident Tests.

Determining whether someone is a UK tax resident or non-UK resident is essential for establishing their tax liability. HMRC uses a clear set of criteria called the Statutory Residence Test (SRT). This blog outlines these rules, explains how the tests work, and provides a practical example to clarify how they apply in real life.

Why Residency Matters

Your UK residency status affects how much tax you pay and on which income. If you are a UK resident, HMRC taxes your worldwide income. On the other hand, if you are non-UK resident, you are generally taxed only on your UK income.

Determining your UK residency status is essential for tax purposes. The UK tax system has specific rules to classify individuals as residents or non-residents. These rules influence how much UK tax you pay on your global income and gains. This guide breaks down the UK Resident and Non-UK Resident Tests, helping you navigate this critical area.

What Are the UK Residency Rules?

The Statutory Residence Test (SRT) determines whether you are a UK resident or not for tax purposes. Introduced in 2013, this test provides a clear framework based on:

- Days spent in the UK

- Your connections to the UK

- Specific situations or activities

To establish your residency, the SRT examines three main areas:

- Automatic Overseas Test

- Automatic UK Test

- Sufficient Ties Test

Let’s explore these in detail.

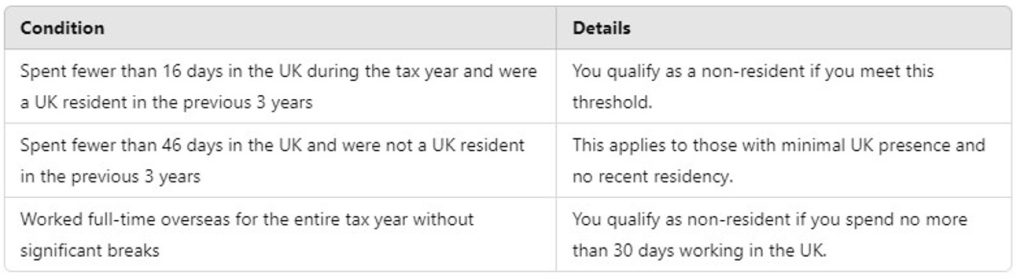

1. Automatic Overseas Test

You are automatically non-UK resident if any of the following apply:

– You were resident in the UK for one or more of the previous three tax years, and you spend fewer than 16 days in the UK in the current tax year.

– You were not resident in the UK in the previous three tax years, and you spend fewer than 46 days in the UK in the current tax year.

– You work full-time abroad and spend fewer than 91 days in the UK, of which no more than 30 days are work days.

2. Automatic UK Test

You are automatically UK resident if any of the following apply:

– You spend 183 days or more in the UK in a tax year.

– You have a UK home where you stay for at least 30 days and you are present in that home for at least 30 days in the tax year.

– You work full-time in the UK for any period of 365 days, and at least one day of that work falls within the tax year.

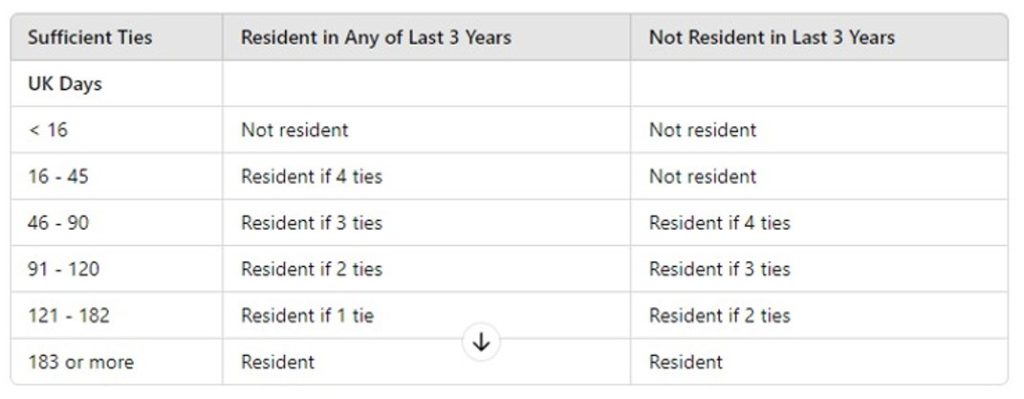

3. Sufficient Ties Test

If you do not meet any automatic test, you need to apply the Sufficient Ties Test.

This test counts the number of ties you have with the UK and the number of days you spend in the country. Key ties include:

– Family Tie: Spouse or minor children in the UK.

– Accommodation Tie: Accessible accommodation in the UK.

– Work Tie: At least 40 days of work in the UK.

– 90-Day Tie: You were in the UK for more than 90 days in either of the last two tax years.

– Country Tie: The UK is the country you spent the most days in during the tax year (applies only if you were UK resident in one of the previous three years).

The more ties you have, the fewer days you can spend in the UK without becoming a resident

Let’s consider an example:

David is a UK citizen working for a company in Doha. He moved abroad on 1 May 2023 and plans to stay for at least three years. In the 2024/25 tax year,

– he Spends 40 days visiting family in the UK.

– Has accommodation in London.

– His wife and children remain in the UK.

– He does not work during his UK visits.

David does not pass the Automatic Overseas Test as he spends more than 45 days in the UK. He does not meet the Automatic UK Test either because he doesn’t stay for 183+ days, and does not work full-time in the UK.

Now, we apply the Sufficient Ties Test:

– Family Tie: Yes.

– Accommodation Tie: Yes.

– 90-Day Tie: Yes (he lived in the UK in the previous tax year).

– Work Tie: No.

– Country Tie: No (spent most time in oversea).

He has three UK ties. As a former UK resident, if he has three ties, the day limit for non-residency is less than 91 days. Since he spent only 40 days in the UK, David is non-UK resident for tax purposes in 2024/25.

Planning Tips for Tax Status

– Keep accurate records of your travel days.

– Track your UK ties annually.

– Consider the impact of short visits on your residency.

– Speak to a tax adviser if your situation is complex or if you’re moving abroad.

Split-Year Treatment

In some cases, you may not be resident for the full year. Split-year treatment applies when you leave or arrive in the UK partway through a tax year. It ensures you’re taxed as a resident only for the relevant part of the year. There are eight cases under which this may apply — such as starting full-time work abroad or ceasing to have a UK home.

Double Taxation Agreements (DTA)

If you’re taxed in both the UK and another country, you may claim relief under a Double Taxation Agreement. The treaty outlines which country has taxing rights and avoids double taxation on the same income.

Conclusion

Understanding the UK Resident and Non-UK Resident Tests is key to managing your tax obligations correctly. The Statutory Residence Test provides a clear structure, but applying it can still be complex — especially when multiple ties are involved. Keeping good records and being aware of your travel patterns will help you stay compliant and possibly avoid unnecessary tax liabilities.

If you would like further assistance with this or anything else, please get in touch, contact us for expert assistance.